All-Weather Strategy

Risk Parity v2.1 - Asymmetric Mean-Reversion

Overview

| Company: Infinity Capital Management | Role: Quantitative Researcher Intern | Period: Mar-Jul 2024 |

Implementation of Ray Dalio’s All Weather Strategy with Ledoit-Wolf covariance shrinkage and asymmetric mean-reversion (v2.1).

Key Results:

- Sharpe Ratio: 1.11 (backtest 2018-2026)

- Max Drawdown: -6.83%

- Total Return: +93%

- Live tracking since Jan 2026

Methodology

Risk parity allocates by risk contribution rather than capital, ensuring each asset contributes equally to portfolio volatility. This provides true diversification since traditional portfolios are dominated by equity risk.

Key Features:

- Asymmetric thresholds: 3% trim (lock gains early) / 10% buy (patient on dips)

- Daily drift checking: Per-asset rebalancing when thresholds breached

- Weekly optimization: Target weights updated every Monday via risk parity

Process:

- Estimate covariance using Ledoit-Wolf shrinkage (252-day lookback)

- Optimize weights for equal risk contribution

- Daily monitoring with asymmetric drift thresholds

- Transaction cost modeling (0.03%)

Results

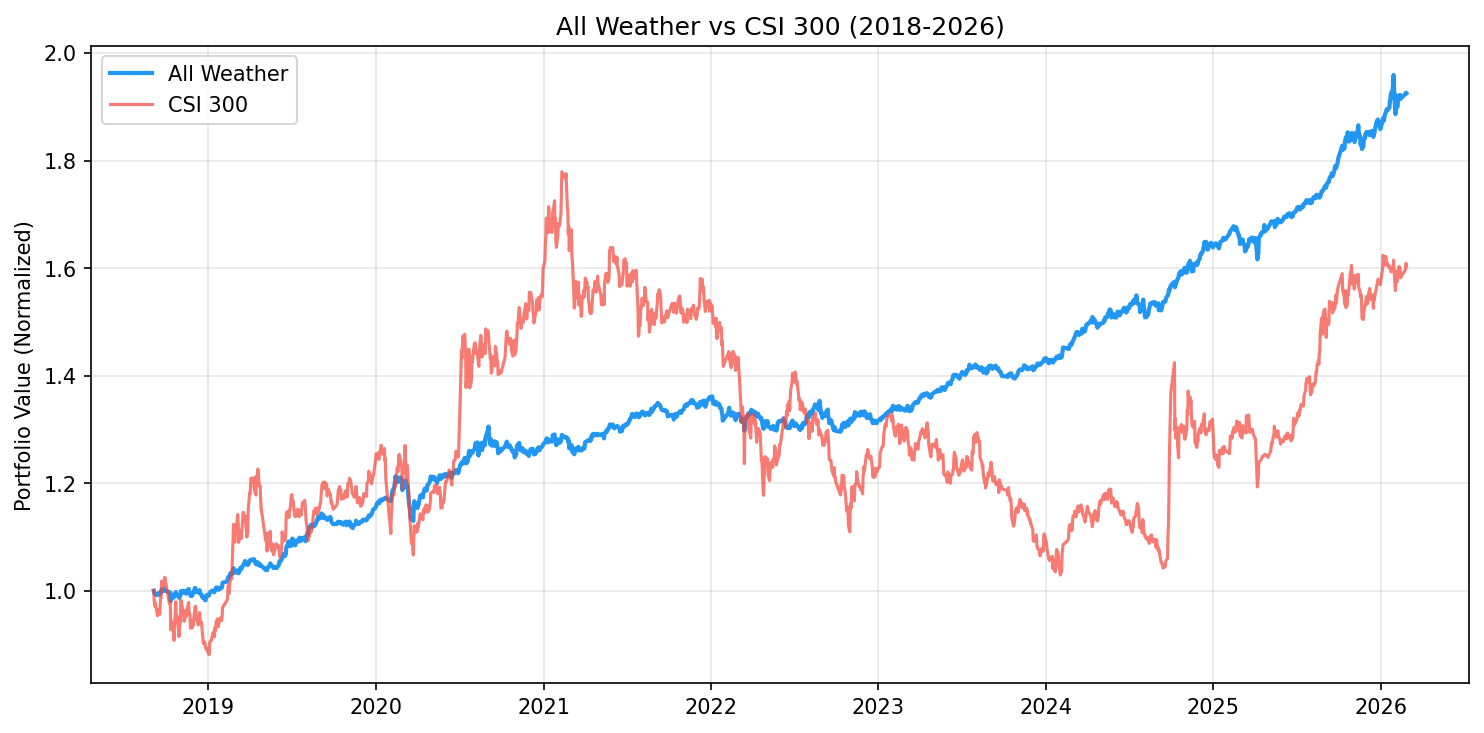

Equity Curve

The All Weather portfolio returns +93% over the 2018-2026 backtest period, significantly outperforming the CSI 300 benchmark. The strategy delivers smoother growth with max drawdown of -6.83%, compared to the benchmark’s much deeper drawdowns during market corrections.

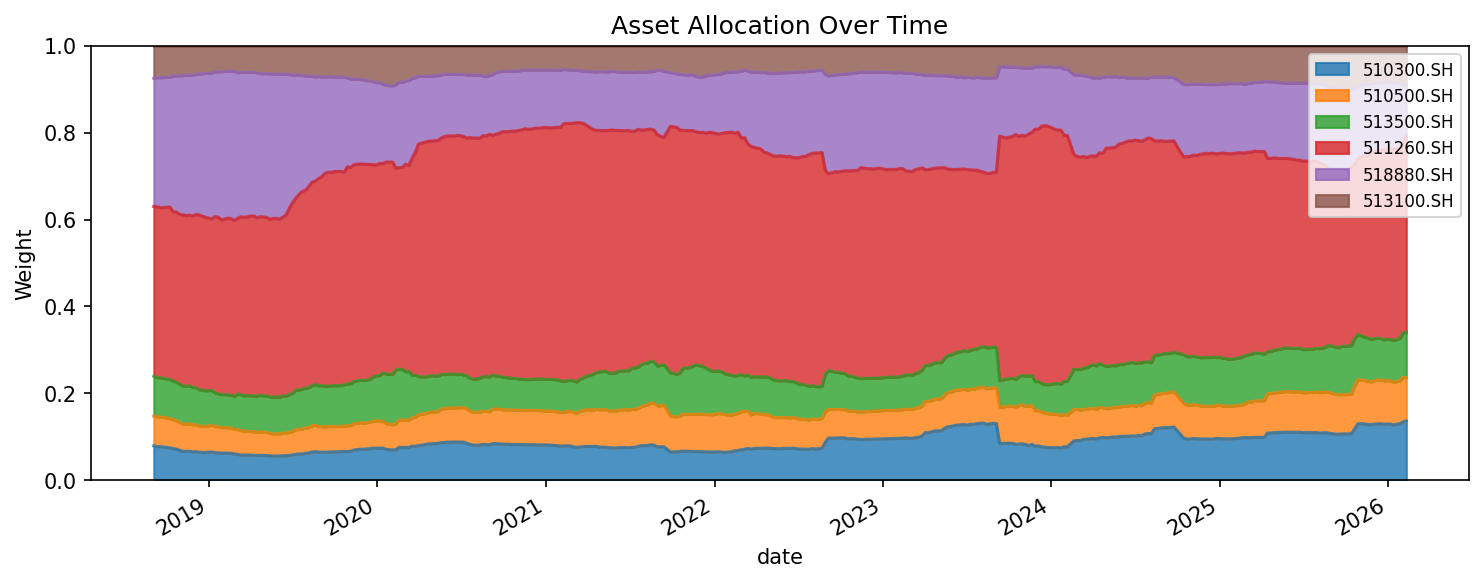

Asset Allocation

Risk parity naturally allocates ~70% to government bonds, which carry low volatility but contribute equal risk to equities and commodities. The weights remain stable over time, with only gradual shifts as cross-asset correlations evolve.

Tech Stack

Python, NumPy, pandas, scipy (optimization), Ledoit-Wolf shrinkage

Live Strategy Tracker (2026)

Loading...